We’ve all been there — out on a Saturday, bracing yourself as you think about the chaos that lies ahead as you need to run to … Costco.

Packed parking lots, concrete floors, disorganized aisles, long lines, and multiple receipt checks are all part of the Costco experience. While this may not sound appealing at first, millions of American families have decided that Costco’s slight inconveniences are well worth the potential savings. With prices for hundreds of grocery items increasing more than 50% since 2019, it’s no surprise Costco memberships have skyrocketed.

And while the recent news of Costco raising membership fees for the first time in seven years may be surprising, the continuing rise of health plans costs isn’t.

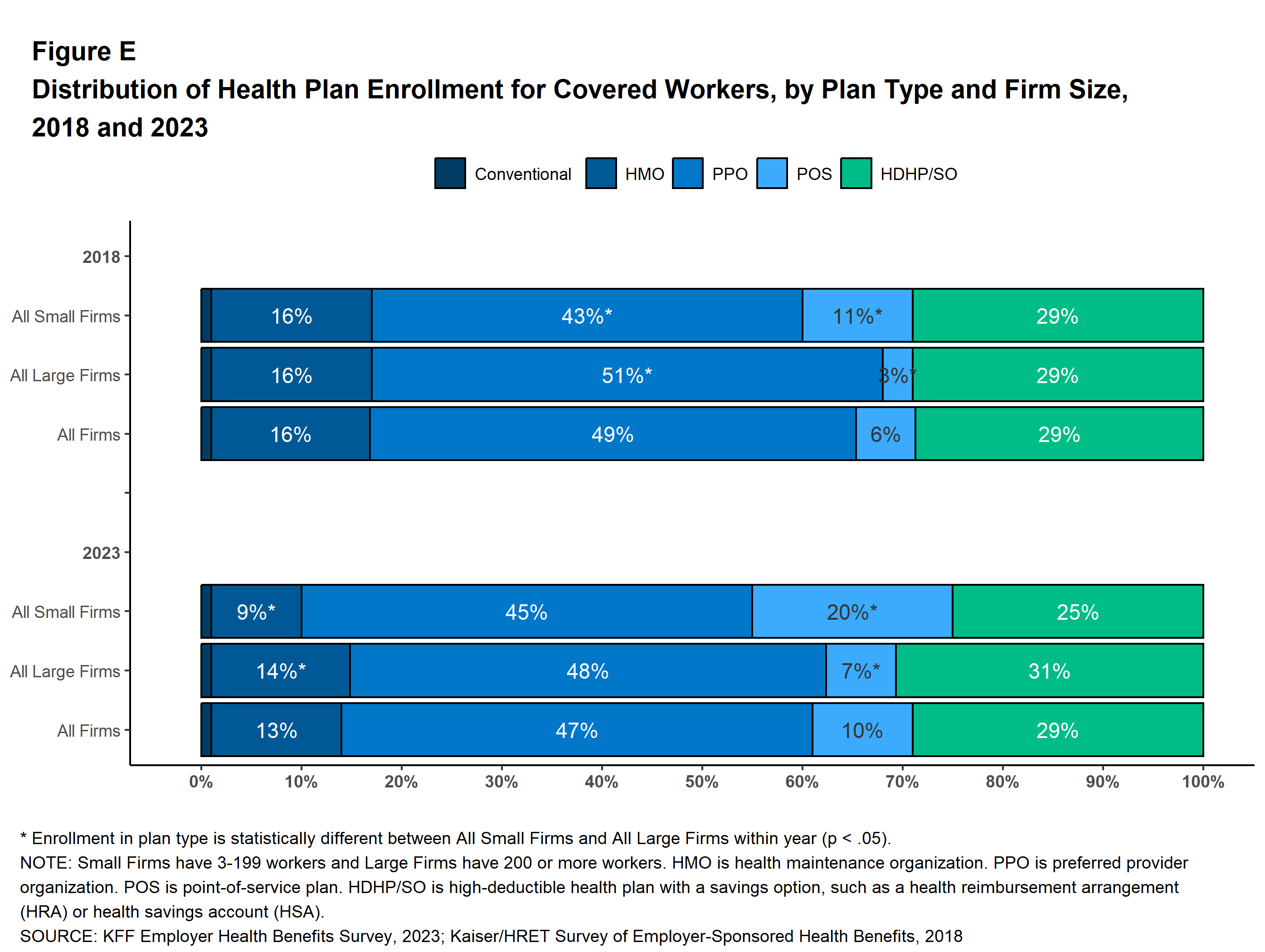

Today, approximately 47% of working Americans are enrolled in a Preferred Provider Organization (PPO) plan through their employer. PPO plans are known for providing convenient access to a broad network of doctors where members can enter a facility or doctor’s office, show their insurance card, and walk right into the exam room. However, this convenience comes at a cost.

{kind=link}

Just like it’s more expensive to shop at your local Target, PPO plans are significantly more costly, and the choice to enroll nearly half of working Americans in a PPO drives up the total cost of care. According to the Kaiser Family Foundation, the average annual insurance premium for family coverage under an employer was a staggering $23,968 – nearly 370 annual Costco memberships. With a median salary nationwide of $48,060, this simply isn’t sustainable. Even worse, more than 40% of Americans are experiencing medical debt and annual premiums are expected to increase, on top of out-of-pocket expenses for deductibles, copayments and coinsurance.

The path forward is clear: employers must evaluate their health plan the same way they do their Saturday shopping excursion. Unfortunately, most companies are stuck in the status quo and a recent Mercer study found that employers are hesitant to explore alternative health plans options due to disruption concerns.

As CEO of Imagine360, I hear similar concerns from self-funded employers. The last thing they want is to hear that an employee can no longer see their long-time doctor. My answer is simple: if your employee is willing to drive further to Costco to save a few hundred dollars, don’t you think they would be willing to drive to another high-quality provider if it meant saving thousands of dollars on healthcare?

I’m not alone in this thinking. Approaching 2025, Mercer recommends employers focus on creating affordable healthcare benefits and explore alternative network options that steer members into similarly high-quality, yet more affordable, providers rather than focusing on convenience.

I’ve seen this approach play out firsthand. Imagine360 offers many of our self-funded employer clients a dual-option health plan. Employees can choose between a traditional PPO plan or an alternative health plan including preferred provider contracting and reference-based pricing. We explain the alternative health plan may require employees to take an extra step in their healthcare experience, like calling member support to schedule an appointment or discuss preferred doctors in advance, in exchange for significantly lower monthly premiums and out-of-pocket costs.

Let me share an example of how this played out for one employer in the manufacturing industry. Following the first year of the dual option offering, nearly 74% of employees were enrolled under the alternative health plan. This led to substantial savings for the employer and its employees, and our satisfaction rates among these members were above 95%.

With the 2025 open enrollment period beginning in a few months, employers will soon face their own Saturday shopping moment. Will they become more engaged and informed about alternative health plans that offer savings? Or will they continue to offer the convenient, yet often unaffordable, option?

I fully believe that healthcare is ready for its Costco moment.