Historically, payers and providers have shared an antagonistic relationship premised on providers wanting to be paid more for the services and procedures they offer while payers wanted to pay the least amount possible for those very same things.

With the passage of the Affordable Care Act and the strategic move toward value-based care, those lines separating the two have begun to blur a little with ongoing payer-provider integration. Still, a new national survey reveals the chasm that remains between these top healthcare stakeholders. Be it consumerism or interoperability, payers and providers are not seeing eye to eye. And when it comes to value-based care, there is a big disconnect between the two. But there are areas, like social determinants of health, where there are consensus and alignment between the two.

Closing the Quality-Affordability Gap in Workplace Mental Health

In an interview, Kyan Health Co-Founder and Chief Commercial Officer Konstantin Struck discussed how Kyan gives mid-market and enterprise employers access to premium workforce mental healthcare, at a price point that is affordable.

That’s the result of the 2020 Industry Pulse Report, a national survey commissioned by Change Healthcare and the Healthcare Executive Group and conducted annually. The 2020 study was conducted online by market research and strategy firm InsightDynamo.

This year, 445 responses came of which 30 percent were from provider organizations be it hospitals, clinic or doctor’s office and integrated delivery networks. Less that 30 percent were from those employed by payers.

“In our 10 years of fielding this research, I don’t think we’ve seen healthcare industry leaders so polarized on some strategic issues and so tightly aligned on others,” said David Gallegos, SVP, Consulting Services, at Change Healthcare in a news release. “These insights can help foster a dialogue between payers and providers about their priorities, driving collaboration to advance solutions on those issues in the year ahead.”

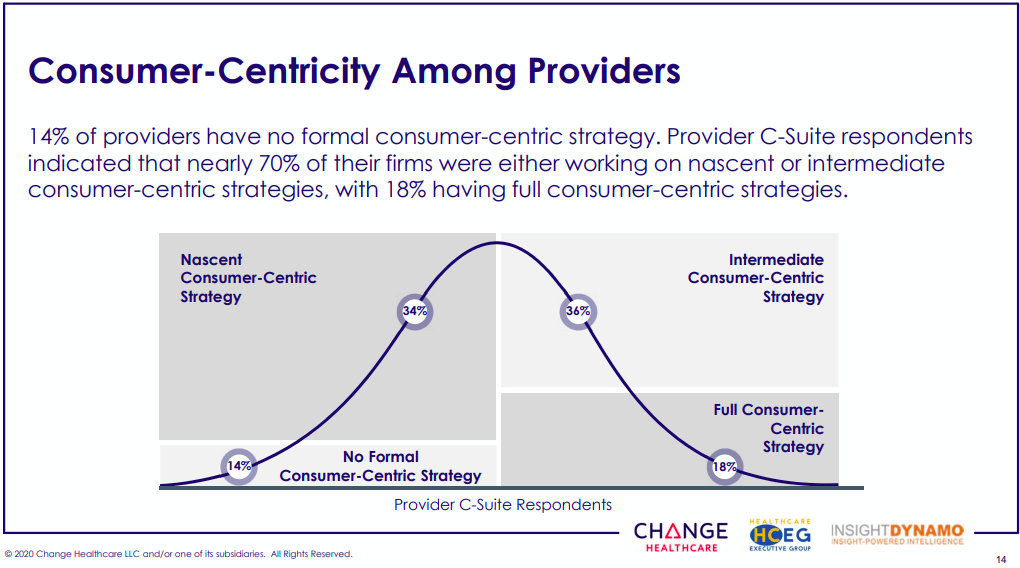

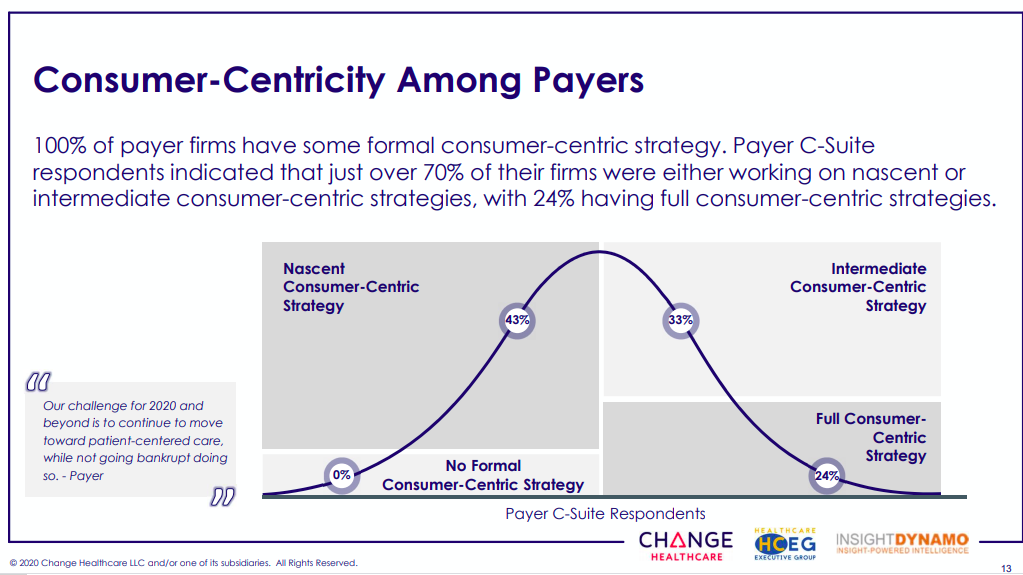

The dialogue should perhaps begin on how the two sides differ on consumerism. Whereas 100 percent of payers said they had some kind of consumer-centric strategies, 14 percent of providers appear to have no consumer-centric strategy all.

Top 7 Modern AI-Powered EAP Providers for Global Workforces in 2026

Discover the top AI-powered EAP providers for 2026. Compare platforms like Kyan Health and Spring Health on triage speed, global reach, and clinical quality to transform workforce wellbeing.

Here’s the continuum of how consumer-centric strategies were described in the survey:

- No Consumer-Centric Strategy – Those that are not currently working on any consumer-centric strategies

- Nascent Consumer-Centric Strategy – Those that have begun to target single-point consumer-centric strategies, but do not have a unified strategy across their organizations.

- Intermediate Consumer-Centric Strategy – Those that have a consumer-centric philosophy and are actively investing in tools and technologies, but have not yet measured company-wide impact or benefits.

- Full Consumer-Centric Strategy – Those that have fully implemented tools and technologies to achieve consumer-centric outcomes, and have effectively measured improvements related to these efforts.

Here’s how providers responded based on the above definitions:

Meanwhile, payers seemed to be much further along on the path to developing consumer-centric experiences.

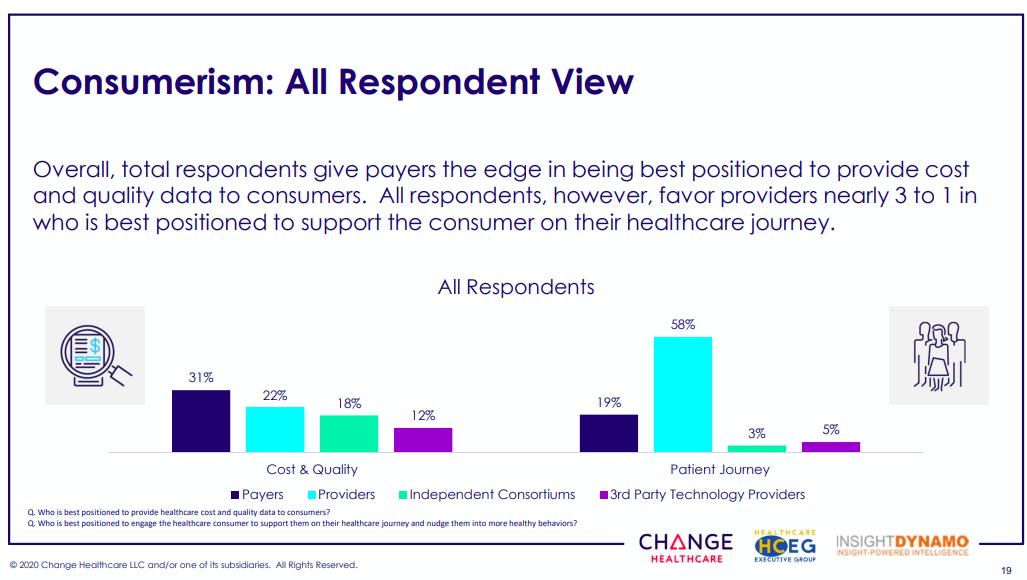

Interestingly, when all respondents — that included tech vendors, healthcare consultants, third-party administrators and others – were asked about who can best deliver on consumer-centric strategies, the answers were mixed on whether the no. 1 would be a payer or provider. When it came to delivering patient cost and quality data, all respondents gave the edge to payers. But when they were asked regarding who can best deliver on the patient journey, perhaps unsurprisingly the answer was providers.

Whereas the results were split when all respondents were asked who can best deliver on consumerism, providers and payers (to some extent) think they alone can deliver on this promise of consumerism. In other words, most providers felt they were in a better position to deliver on consumerism whether it be cost and quality data or patient journey. Payers said they could deliver on the former, but conceded that providers were better positioned to deliver on the patient journey front.

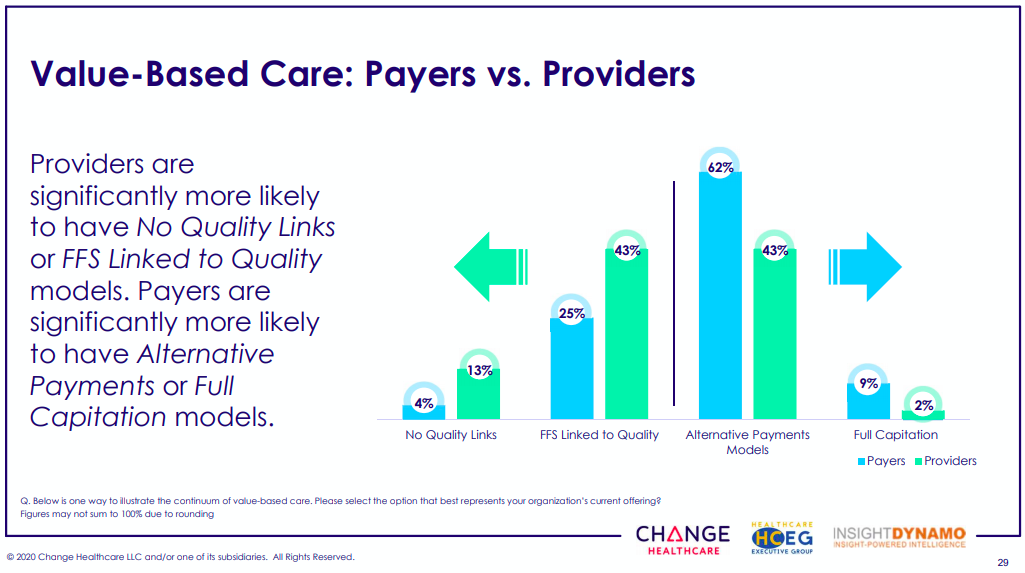

Value-based care was another area where there is a big disconnect between payers and providers. Providers still live in the fee-for-service world where payments are either linked to no quality measures or where fee-for-service payments have some links to quality whereas payers are more fully embracing alternative payment models or full capitation.

The differences were even more pronounced when C-suite execs were surveyed on this.

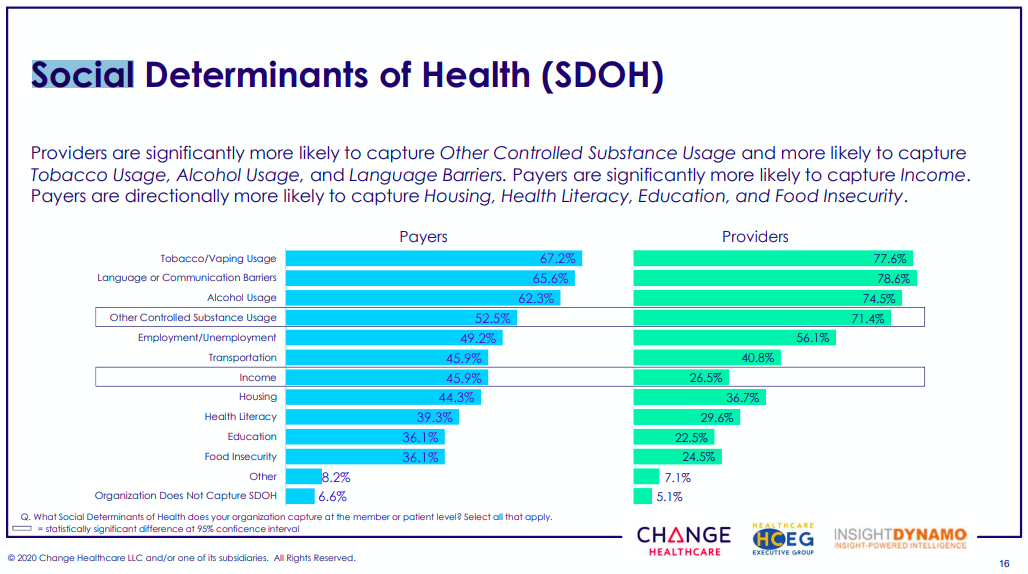

However, these differences notwithstanding, the survey found that payers and providers were heavily aligned on social determinants of health, AI and tactics to improve consumer engagement.

The full report is available here.