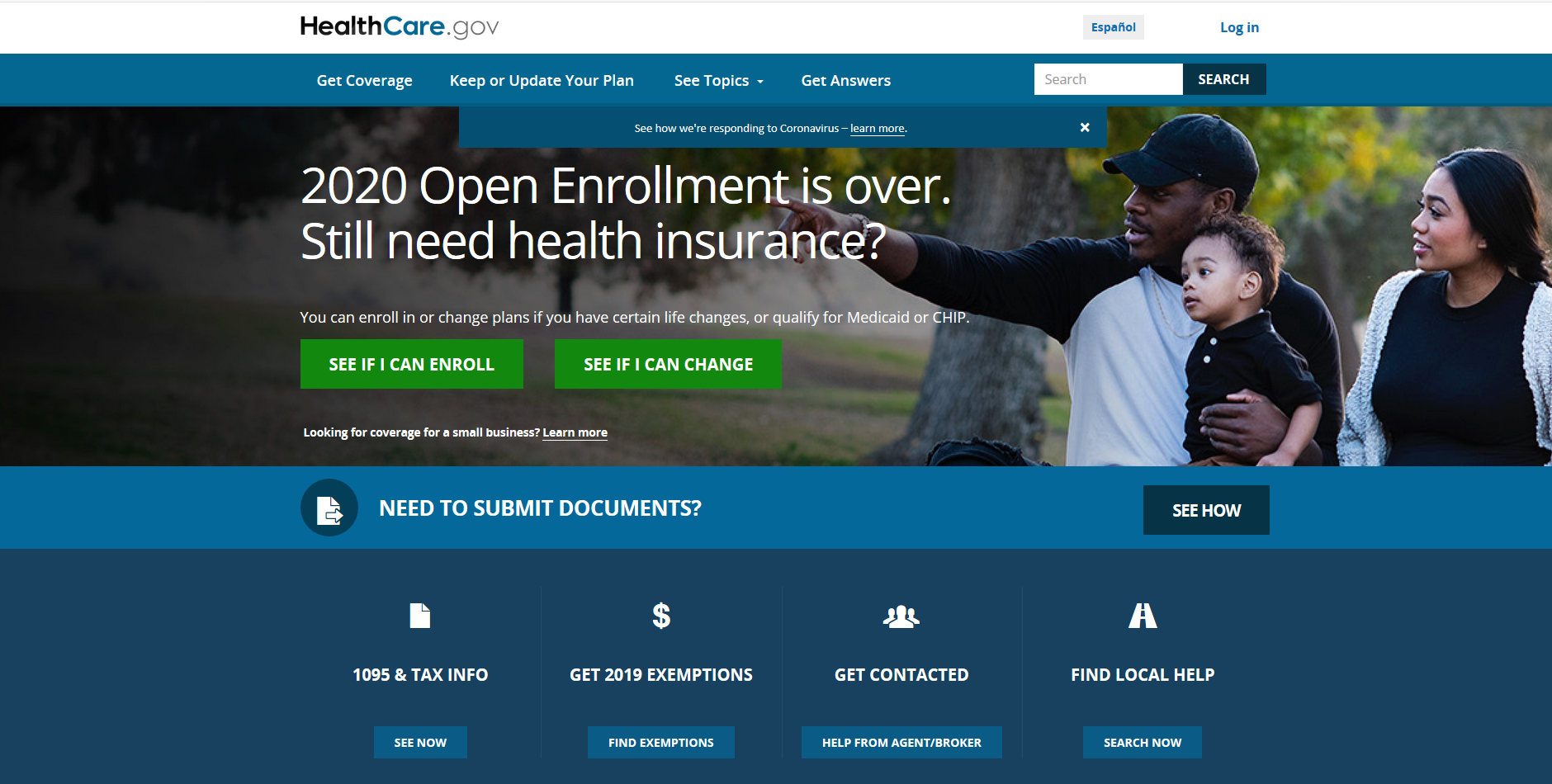

Healthcare.gov has not reopened to allow those without insurance to enroll for coverage in light of the Covid-19 pandemic. Screenshot taken on April 2.

Last week, the number of U.S. residents filing for unemployment soared to new highs, as many businesses shutter or cut staff as a result of the ongoing Covid-19 pandemic. More than 6.65 million people filed claims last week, on top of another 3.3 million claims for the week ending March 21, according to data released by the U.S. Labor Department.

Inside an Automated Healthcare Practice: Redesigning Care Around People, Not Paperwork

By reducing administrative burden and redesigning workflows around human needs, it creates space for what matters most: connection between clinicians and patients.

Many of them will be seeking health insurance, whether through insurance marketplaces established under the Affordable Care Act, Medicaid, COBRA, or even private plans. Households that have some income may be able to enroll in marketplace plans, while those with none would generally be covered under Medicaid. But some people will run into challenges in finding coverage, particularly those in states that have not expanded Medicaid coverage, and those who were already uninsured.

For the latter, the Trump administration said this week that it would not reopen enrollment on Healthcare.gov, which would allow those who had been previously uninsured to enroll in plans through the federal exchanges. Those who just lost their jobs will still be able to enroll for coverage, but a special enrollment period would have also made it easier for them, by requiring less paperwork to prove that they had lost coverage.

The administration has been “exploring other options,” according to Politico, but they’ve still offered no details on what those plans would entail.

At a White House press briefing on Wednesday, Vice President Mike Pence fumbled the question when asked by a reporter about plans for the uninsured.

Closing the Quality-Affordability Gap in Workplace Mental Health

In an interview, Kyan Health Co-Founder and Chief Commercial Officer Konstantin Struck discussed how Kyan gives mid-market and enterprise employers access to premium workforce mental healthcare, at a price point that is affordable.

“All across America we have Medicaid for uninsured Americans,” he said, but failed to acknowledge states where unemployed adults cannot get coverage through Medicaid.

When asked if that coverage would be expanded to the middle class, Pence had no answer.

“One of the things that has animated and characterized the president’s approach is the way he has engaged businesses to step up and do their part,” he said. “I fully expect that we’ll see more of that for people that have insurance. We’ll continue provide flexibility for Medicaid for people that don’t have insurance.”

“It’s something we’re going to look at because it doesn’t seem fair,” President Donald Trump finally said, adding, “I think that’s one of the greatest answers I’ve ever heard, because Mike was able to speak for five minutes and not even touch your question.”

State preparations

States that operate their own insurance marketplaces have opened special enrollment periods to make it easier for residents to enroll. For example, California opened a special enrollment period starting on March 20 for its health insurance marketplace, Covered California.

A spokesperson for Covered California said it saw twice as many special enrollments in March as it has seen previously. But it’s hard to know exactly how many of those stem from the pandemic, as the state had opened another special enrollment period in mid-February.

As for the state’s Medicaid program, Medi-Cal, California does not yet have enrollment data from last month, which is reported in to the state from its counties. Generally, households that lost insurance but still have some income would be able to enroll through Covered California, while a family of three would have to make less than $27,821 to be covered under Medi-Cal.

Adults in states with more restrictive Medicaid policies, such as Texas, Florida and Kansas, may not be able to receive coverage. In these states, coverage is generally restricted to low-income families with children, and adults who have a disability or who are over age 65. In Kansas, lawmakers worked earlier this year to develop a bipartisan bill for Medicaid expansion, but it still hasn’t passed.

Keeping a former employer’s insurance plans through COBRA would be the most expensive option. According to the Kaiser Family Foundation, the average annual premium for employer-sponsored health insurance last year was $7,188 for individuals and $20,576 for families.