Despite the global pandemic, enterprise health systems have moved beyond “all Covid all the time” and are actively seeking new commercial relationships with health tech startups. However, given strained budgets, the bar for startups just went up a few notches.

That’s the takeaway from a survey of 20 health system CIOs and innovation leaders from across the country which sought to examine how Covid-19 has impacted budgets, when normalcy is expected, and which problems need urgent solutions.

The Healthcare Payments Industry Faces a Perception Challenge

Healthcare payments are no longer about transactions. It’s about controlling the revenue cycle. And increasingly, that control is not sitting with ISOs.

Dreamit Ventures and MedCityNews teamed up to get a pulse on the current appetite for innovation at large health systems across the United States. The survey data tapped senior innovation leaders, 85% of whom came from health systems with over 1,000 beds. Notable health systems surveyed include Kaiser Permanente, Houston Methodist Hospital, University Hospitals, Thomas Jefferson, Children’s Hospital of Los Angeles, Duke University, and St. Luke’s University Health Network, among others.

During the first three-quarters of 202o, most major health systems were primarily interested in engaging with companies whose platforms had compelling Covid–19 use cases that could be immediately deployed. However, health systems today appear to have moved beyond the all-consuming focus on Covid-19. This should come as welcome news for health tech startups. Large health systems are once again actively exploring new commercial relationships with these upstarts, seeking platforms that solve big and urgent challenges that existed well before the pandemic. Only one health system reported exclusive interest in direct Covid-19 solutions.

During the first three-quarters of 202o, most major health systems were primarily interested in engaging with companies whose platforms had compelling Covid–19 use cases that could be immediately deployed. However, health systems today appear to have moved beyond the all-consuming focus on Covid-19. This should come as welcome news for health tech startups. Large health systems are once again actively exploring new commercial relationships with these upstarts, seeking platforms that solve big and urgent challenges that existed well before the pandemic. Only one health system reported exclusive interest in direct Covid-19 solutions.

The survey was geographically diverse with responses coming from across the nation. Click the map to enlarge.

Top 7 Modern AI-Powered EAP Providers for Global Workforces in 2026

Discover the top AI-powered EAP providers for 2026. Compare platforms like Kyan Health and Spring Health on triage speed, global reach, and clinical quality to transform workforce wellbeing.

One clear and recurring theme was the focus on limited budgets and platforms that can demonstrate an immediate and defendable ROI. The majority of large health systems are even more selective and have decreased or frozen operating budgets.

“This is not surprising since major health systems incurred billions in losses when profitable elective procedures were suspended,” said one innovation leader who declined to be identified directly.

This sentiment was echoed by Matthew Fenty, Director of Innovation & Strategic Partnerships at St. Luke’s University Health Network.

“Strategic capital has been, generally, frozen to manage cash-flow issues which arose this year,” he said.

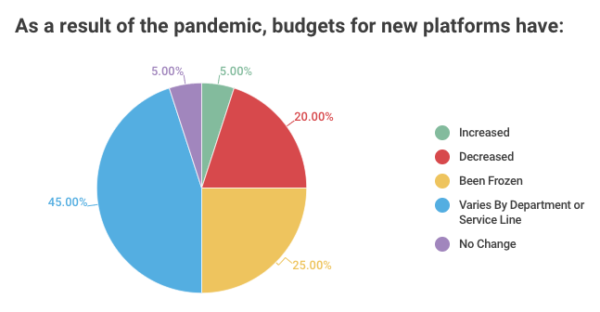

Nearly half of large health systems reported that budgets for new innovations have been frozen or decreased across the board. Only 10% of large provider systems reported increased or stable budgets since the pandemic. However, results vary depending on what budget you sell into – 45% of health systems saw budget impacts vary by department or service line.

This strain on budgets necessarily means that the bar for startups is going higher. Fewer startups are likely to pass newer tougher screening criteria, and only those that can support a clear and immediate ROI are likely to get traction.

Todd Dunn, vice president of innovation and innovator-in-residence at Atrium, was likely commenting on behalf of many hospital leaders when he shared his skepticism for startups with ROI projections with no basis in reality.

“[It’s] just surprising how many startups present ROI stories with minimal data that either lack credibility or are simply based on weak or unproven assumptions. Feels like the ROI slide is often just a placeholder in their deck,” he said. “This is all about cost, and I mean COST in capital letters.”

While 95% of respondents indicated they are actively engaging in new partnerships, this stands in contrast to the pandemic’s impact on budgets, which have clearly taken a hit at large health systems.

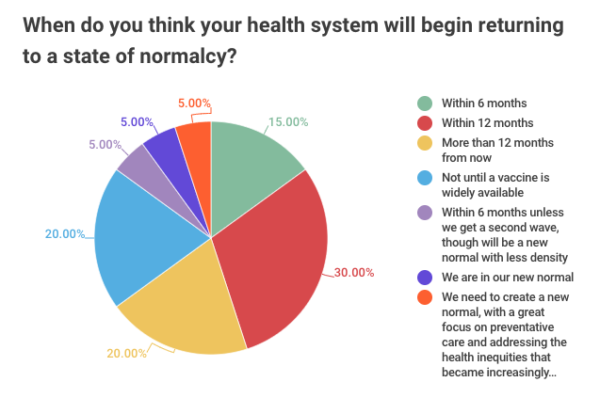

The question remains: When will budgets return to pre-Covid-19 levels? The jury is still out. Near equal numbers felt normalcy would come within 12 months (30%), over 1 year from now (20%), or would be contingent on the widespread distribution of a vaccine (20%). Only 15% of health systems felt normalcy will return in the next six months. While innovation leaders were split on how long the pandemic will last, only 5% of systems felt the current environment is the “new normal”.

The common belief is that operations are beginning to return to pre-pandemic levels, though most feel expanded telehealth is here to stay. Two-thirds of health systems felt they would increase or maintain current levels of telehealth activity beyond the pandemic. While 30% predict a slight shift back towards in-person, only 5% predict a significant shift away from telehealth.

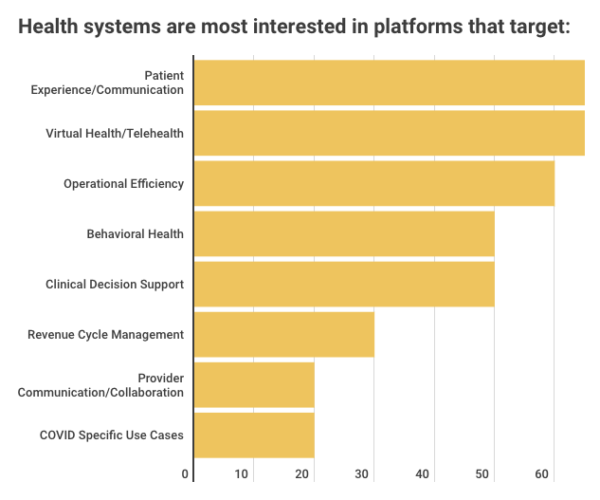

Telehealth, patient engagement/communication, and operational efficiency are the most pressing priorities for innovation leaders at large health systems (64% reported interest). The intense focus on Covid-19 appears to be waning with only 20% of respondents looking solely for pandemic solutions. While Covid-19 is still rising in many parts of the country, this suggests that health systems have gotten to a place where they feel they now have the infrastructure to manage the pandemic. Not far down the list are other priority areas like behavioral health (which was a hot funding area through Q2 2020), clinical decision support, and revenue cycle management.

Telehealth, patient engagement/communication, and operational efficiency are the most pressing priorities for innovation leaders at large health systems (64% reported interest). The intense focus on Covid-19 appears to be waning with only 20% of respondents looking solely for pandemic solutions. While Covid-19 is still rising in many parts of the country, this suggests that health systems have gotten to a place where they feel they now have the infrastructure to manage the pandemic. Not far down the list are other priority areas like behavioral health (which was a hot funding area through Q2 2020), clinical decision support, and revenue cycle management.

These findings present an optimistic outlook on the current appetite for new health tech innovation at large health systems. While budgets have contracted, the need to solve big and urgent problems with innovation remains strong. Health system leaders are actively seeking new commercial relationships with startups regardless of when “normal” returns. However, to win new business in this environment, health tech entrepreneurs must appreciate more than ever before that not only will solutions need to be on the shortlist of priorities, but also data supporting a clear ROI is mandatory. Health tech startups that align with strategic priorities and understand the math behind their value propositions will find that the unprecedented challenges we now face are all also creating unprecedented opportunities.

Photo: ipopba, Getty Images and Dreamit Ventures